HELOC vs. Cash Out Refinance

What are the differences in a HELOC vs. Cash Out Refinance?

Utilizing your home equity can be a good financial solution for many homeowners. If you have owned a home in Texas for at least a few years, you likely hold equity in your home. There are two popular loan options for accessing your equity. A Home Equity Line of Credit and a Cash-Out Refinance loan a structured differently, but both allow you to use your home equity.

Comparing a HELOC vs. a Cash Out Refinance should involve an analysis of what type of loan works best for your needs. The type of lien, loan repayment, interest rate options, and other differences in these loans can help you decide which type of home equity loan you want.

Let’s take a look at the differences between a HELOC and Cash-Out Refinance:

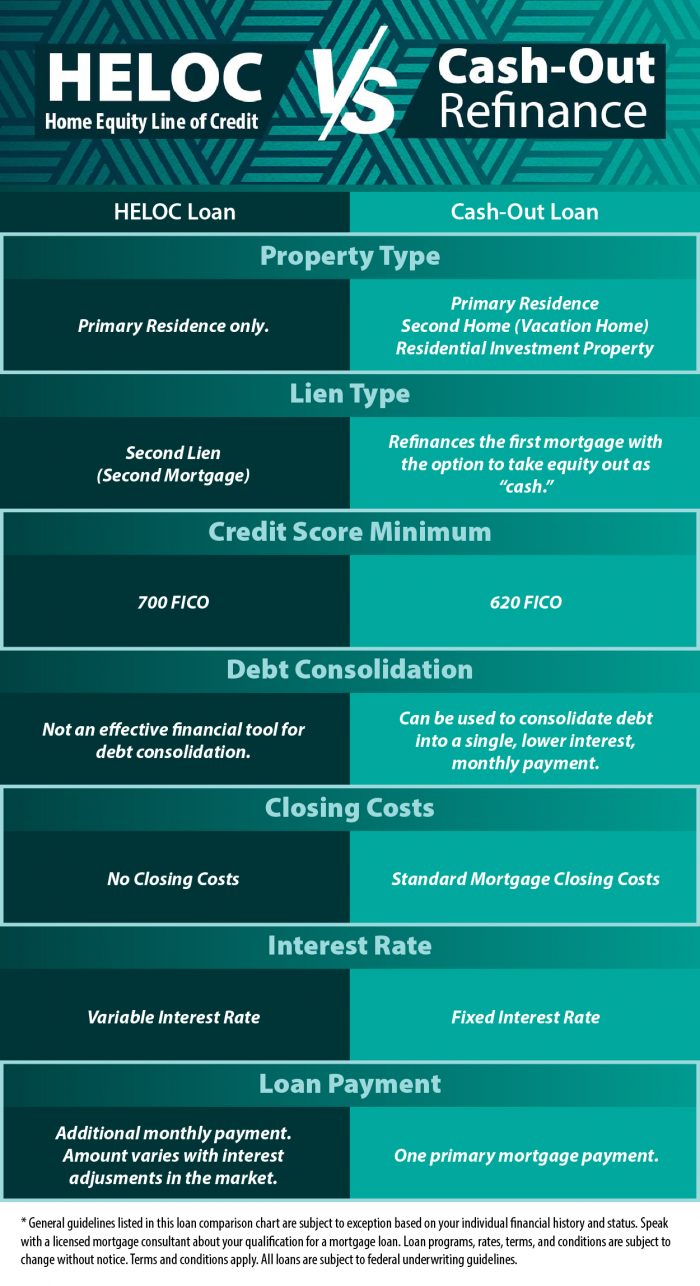

Property Type:

HELOC loans can only be used for your primary residence.

Cash-Out Refinance loans can be utilized to access the equity in your primary residence, a second home (vacation), or an investment property.

Lien Type:

A home equity line of credit is a type of second mortgage. Which means that it is a second lien on your primary residence. Banks often consider 2nd mortgages as higher risk loans and they can come with more strict qualification guidelines.

Cash-out refinance loans are a refinancing of your first mortgage, with the ability to draw cash from your available home equity. You could potentially have the option to adjust or extend the term of your loan.

If you have previously utilized a Cash-Out refinance on your home, Texas mortgage guidelines do not allow you to get a second lien on the same property. There is also a 12 month waiting period for homeowners who have accessed a cash-out loan, before they can apply for another cash out loan on the same property.

Qualifying Credit Score:

A cash out refinance requires a minimum 620 FICO credit score, it is a conventional mortgage loan product. A HELOC loan is considered a higher risk investment for banks and can often require a 700 or higher FICO credit score to qualify.

Debt Consolidation:

Not only does the higher credit score requirement make it more difficult for homeowners to potentially qualify for a HELOC, these loans have more stringent debt to income guidelines.

For homeowners that are looking to pay off high interest credit card debt or other higher interest loans, a Cash Out Refinance loan can be easier to qualify for. Your debt repayment can be off-set in the calculation for the debt to income ratio for a cash out refinance loan. Making cash out refinance loans easier to qualify for when you are looking to consolidate debt.

Many HELOC loans do not allow your debt pay-offs to be calculated in the debt to income qualification guidelines. This is often because your HELOC repayment is an additional monthly payment, and does not reduce portion of your monthly income that is dedicated to debt repayment.

Closing Costs:

One of the attractive aspects of getting a HELOC is having no closing costs. Because a cash-out loan refinances your first mortgage, there are some closing costs associated with closing your loan.

Homeowners who are looking to borrow a smaller amount of money for home renovations often consider a HELOC the better deal. If you are looking to borrow less than $30k from your equity and intend to pay back the borrowed amount quickly, then a HELOC may be what you are looking for.

Although there are no closing costs, HELOCs have a different type of interest and can cost more in the long term. Let’s take look at the structure of the interest for each type of loan below.

Interest Rate:

The majority of HELOC loans are offered with a variable interest rate. Similar to the way that credit card interest is structured, HELOC loan interest can and will change with fluctuations in the market.

Being a second mortgage, HELOC loans are considered to be at a higher risk of default. This can mean that the interest rate available on HELOC loans is often higher.

The interest rate on most cash out refinance loans is fixed. A fixed interest rate, does not change for the entire loan term.

Loan Repayment:

As a second mortgage the monthly payment on a HELOC will be an additional monthly payment, separate from your first mortgage payment. With a variable interest rate, the amount due in interest for your HELOC payment will change over time.

This home equity line of credit will allow you to borrow money during a set amount of time called a “draw period.” During the draw period, minimum monthly payments are applied to the interest on the amount borrowed. At the end of the set draw period you will no longer be able to draw from your equity and your loan will enter the “repayment period.” Payments made during the repayment period are applied to both the principal and interest due on the loan.

By comparison, the loan repayment on a cash out refinance is more steady. The amount of cash borrowed from your equity is rolled into your first mortgage. With a fixed interest rate, the total of the principal and interest portion of your monthly mortgage payment does not change for the life of the loan.

What should I get, HELOC vs. Cash Out Refinance Loan?

Every mortgage and financial outlook is different for each person. Deciding whether a home equity line of credit or a cash out refinance is better suited for your financial needs is something that you should discuss with a licensed mortgage consultant.

We are here to give you a look at your best mortgage options. Our goal is to help you access the best mortgage available to you. Reach out to a mortgage expert on our team with your home equity loan questions today!